Why the Agentic Evolution Preserves Software but Destroys Adobe

The Figma Catastrophe & Canva-Affinity Trojan Horse

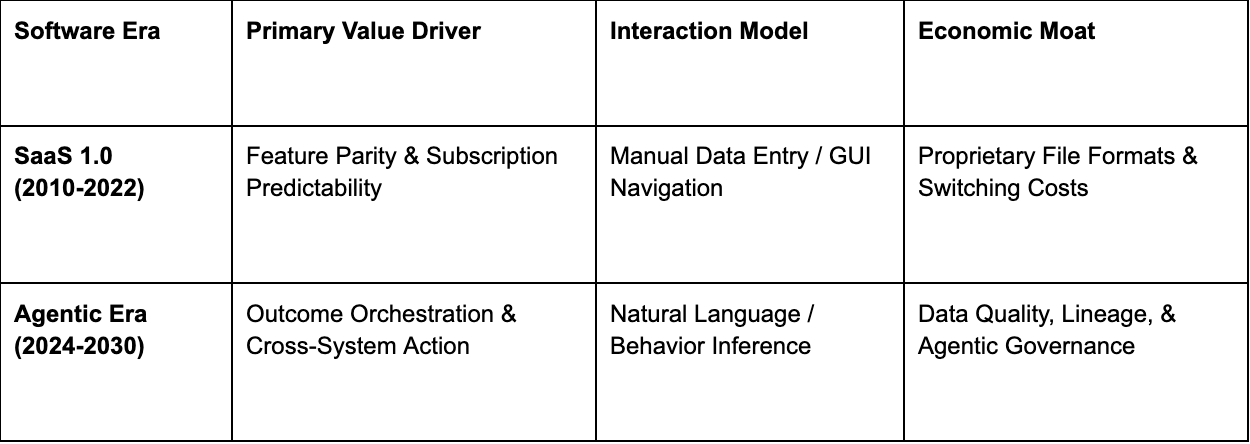

The global software industry is currently navigating a period of profound structural re-architecture, one that has catalyzed a divergent narrative between the category’s fundamental resilience and the specific decay of its legacy incumbents. While a superficial death of software narrative gained traction in the early 2020s, closer inspection reveals that the sector is not vanishing but is instead being subsumed into a more pervasive, agentic operating fabric for the enterprise. The fundamental value proposition of software is shifting from the provision of tools to the orchestration of outcomes.

Within this paradigm shift, Adobe Inc. (ADBE) stands as the quintessential example of an incumbent whose historical competitive advantages—complexity-based switching costs and a digital landlord subscription model—are being systematically dismantled by pricing deflation, specialized AI-native competitors, and a catastrophic failure in strategic capital allocation.

The Structural Resilience of Software and the Myth of Category Obsolescence

The prevailing anxiety regarding the death of software is largely predicated on the rise of generative artificial intelligence and its perceived ability to allow end-users to bypass traditional applications. However, professional analysis of the technology stack suggests that software is entering an era of invisible stack resilience. The primary bottlenecks in the current technological cycle are physical: power generation, data center cooling, and chip availability, rather than a lack of utility for the software layer. In fact, the software category is expanding its role as the operating fabric of the modern enterprise, moving from peripheral use cases to the core layers that shape decisions and strategy execution.

By 2026, the software industry has pivoted toward agentic middleware, where applications no longer act as passive repositories of data but as active participants in end-to-end business processes. This transition represents a move from Human-in-the-Loop (HITL) workflows to Human-on-the-Loop (HOTL) supervision. In this framework, software does not die; it becomes more deeply integrated and indispensable. However, the nature of that software is fundamentally different from the monolithic suites that defined the SaaS era.

The value has moved toward integration layers, data management foundations, and orchestration engines that knit together disparate silos like ERP, CRM, and private banking data.

The resilience of the category is evidenced by the projected doubling of domestic electricity load growth annually over the next decade, driven by the data center requirements of this new software paradigm. As developers shift their focus from building basic applications to architecting, governing, and orchestrating agentic systems, the demand for sophisticated software remains robust. The death is reserved not for software as a whole, but for the digital landlord model that Adobe perfected—a model now besieged by a two-front war of commoditization and specialized disruption.

The Bearish Thesis on Adobe: A Forensic Examination of Moat Erosion

My bearish outlook on Adobe is rooted in the realization that its wide moat—once believed to be entrenched in the professional workflows of millions—is actually a legacy artifact vulnerable to the democratizing power of AI. Adobe’s primary defense has been its Firefly model, which offers commercially safe, indemnified content generation for enterprises. While this provides a temporary legal shield for Fortune 500 clients, it does not address the fundamental erosion of the last mile of creative work.

The core threat to Adobe is that its software has historically been a high-friction, high-complexity destination for creative professionals. AI removes that friction, allowing non-professionals to achieve good enough results and professionals to achieve 10x productivity gains using tools that do not require the steep learning curve of Photoshop or After Effects. This leads to pricing power deflation, where the high monthly subscription fees of the Creative Cloud become a target for procurement departments looking to optimize budgets.

The Financial Decay of an Incumbent

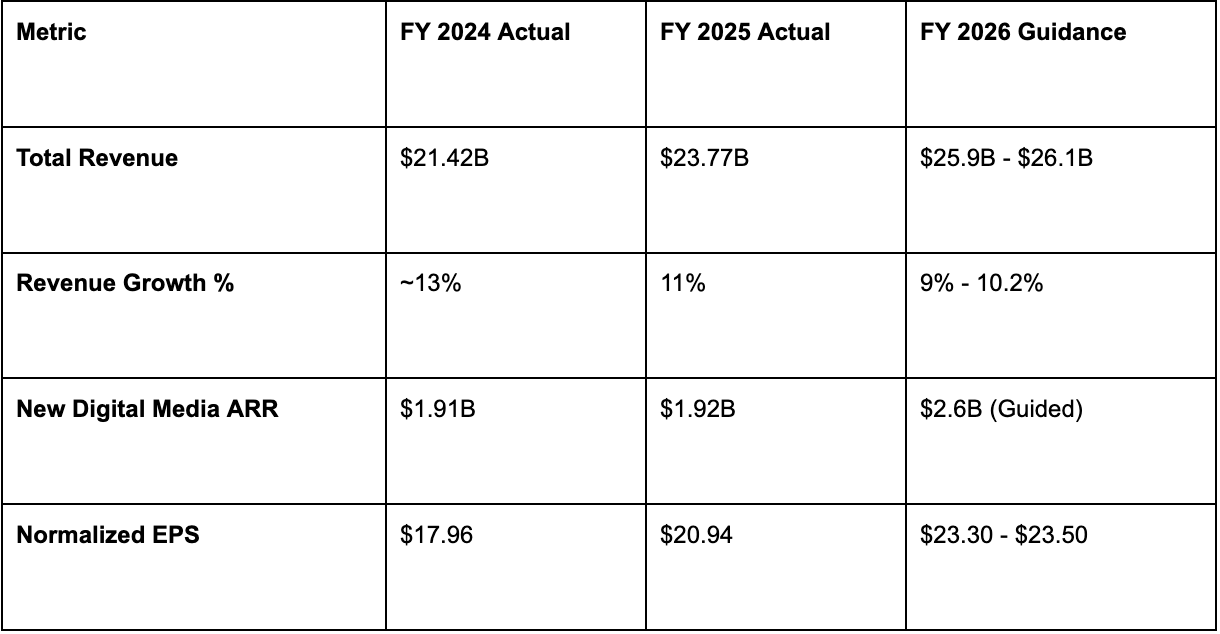

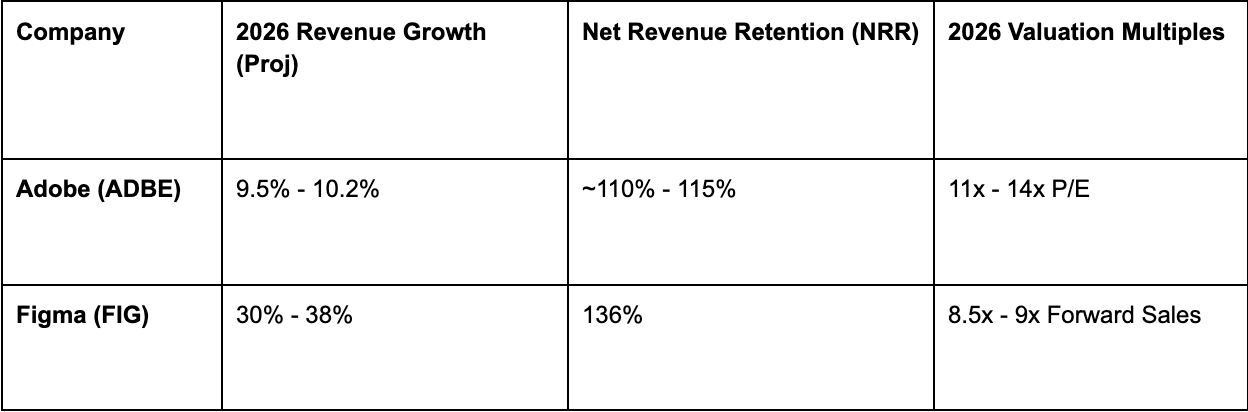

Adobe’s financial metrics for fiscal 2025 and guidance for 2026 reveal a company entering a structural growth slowdown. Revenue growth, which consistently sat in the mid-to-high teens for a decade, has moderated to approximately 10-11% in FY2025 and is guided to fall into the single digits (9.5%) for the first time in recent history. This deceleration is not merely a cyclical headwind but a signal that Adobe is transitioning from a hyper-growth story to a mature, high-quality software company—a transition that justifies a complete reset in valuation multiples. The market’s reaction to this slowdown has been a violent multiple compression. Adobe’s forward price-to-earnings (P/E) multiple has collapsed from a historical range of 30x-40x to approximately 11x-15x by early 2026. This reset indicates that investors are no longer willing to pay a premium for a monopoly that is being disrupted on multiple fronts. Institutional sentiment has soured, with firms like Goldman Sachs and Piper Sandler downgrading the stock based on concerns over revenue durability and the aggressive push from competitors like Figma and Canva.

The Figma Catastrophe: A Strategic and Capital Allocation Failure

The termination of the $20 billion Figma acquisition in December 2023 stands as one of the most significant strategic failures in modern tech history. Regulatory intervention from the UK’s Competition and Markets Authority (CMA) and the European Commission forced the deal’s collapse, citing concerns that the merger would terminate all current and future competition in the collaborative design space.

The fallout for Adobe was multifaceted. First, it was forced to pay a $1 billion reverse termination fee in cash—a record penalty that essentially funded the expansion of its most dangerous rival. Second, it lost the opportunity to own the standard for collaborative UI/UX design, leaving its own tool, Adobe XD, in maintenance mode while Figma became the undisputed industry standard.

The Figma IPO: A What Could Have Been Nightmare

Figma’s public market debut in July 2025 further intensified the bearish sentiment toward Adobe. While Adobe had valued Figma at $20 billion in 2022, Figma’s IPO valuation reached approximately $57 billion, with shares tripling on the first day of trading. This represents $37 billion in unrealized value that Adobe shareholders missed, a figure that is nearly 40% of Adobe’s current market capitalization.

Figma’s 2026 guidance projects revenue growth of 30%, reaching nearly $1.4 billion, with a net revenue retention (NRR) rate of 136% for large customers—metrics that far outshine Adobe’s aging Digital Media segment. Figma is now leveraging its independent public status to introduce “AI credits” and monetization models that directly target Adobe’s professional customer base, further eroding Adobe’s pricing power.

Figma’s dominance in the Fortune 500 is not just about features; it is about the collaborative foundation of modern product design. Adobe’s attempts to retrofit collaboration into its legacy desktop applications have been viewed as tacked on rather than foundational, creating a persistent disadvantage in a world where design is an increasingly distributed and cross-functional process.

The Canva-Affinity Trojan Horse

While Figma attacks Adobe from the high-end enterprise side, Canva is systematically dismantling its prosumer and SMB funnel from the bottom up. Canva has reached a staggering 180 million monthly active users (MAU) and is aggressively moving into the enterprise space with its Canva Enterprise offering.

The strategic pivot came with Canva’s acquisition of Affinity, a suite of professional creative tools. This move is described by industry analysts as a Trojan Horse strategy. By offering pro-grade tools like Affinity Designer and Photo for free to millions of its users, Canva is bridging the chasm between its mainstream audience and the high-end professional market. This shatters the hierarchy that Adobe spent decades building, where Creative Cloud was for professionals and Adobe Express was for consumers.

The Breakdown of the Prosumer Moat

Adobe’s response, Adobe Express, has failed to gain the same level of mindshare as Canva. PeerSpot data from early 2026 shows Canva holding a 10.2% mindshare in the graphic design software category, compared to Adobe Photoshop’s 5.2%. While Adobe Express is often included for free in larger Creative Cloud licenses, users—and especially non-designers—consistently report a preference for Canva’s all-encompassing creative operating system.

The economic implications for Adobe are dire. To defend its market share, Adobe has been forced to increase its advertising spend significantly, reaching $1.4 billion in 2025. This buying of growth is a sign that the brand’s organic pull is weakening. Furthermore, Canva’s success in establishing a hybrid prosumer workflow—where a project can start in professional-grade Affinity and be finished in consumer-grade Canva—is a workflow model that does not exist in the siloed Adobe ecosystem.

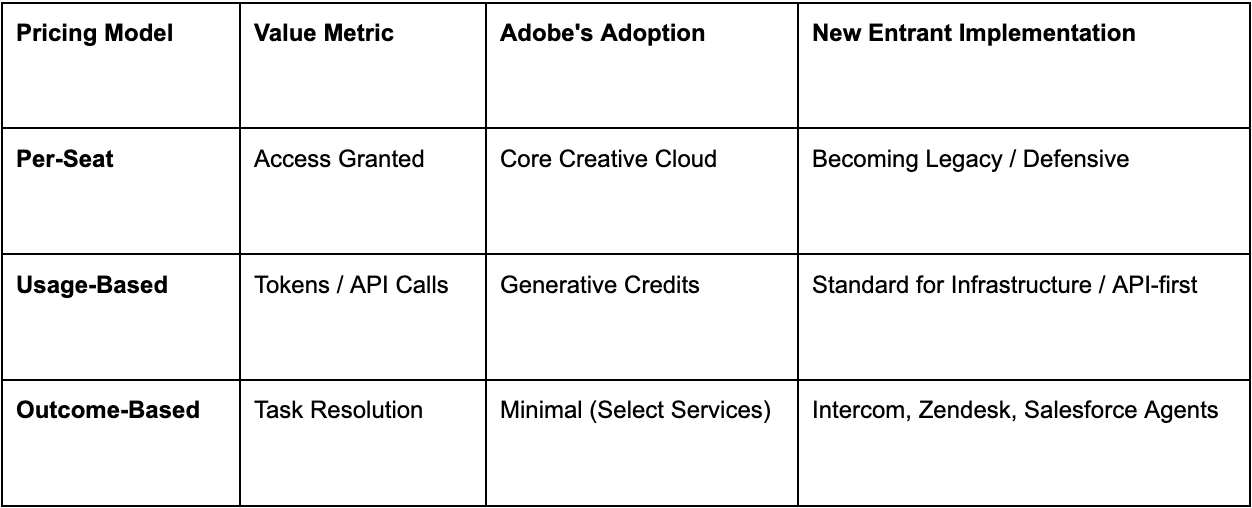

The AI Pricing Crisis: From Seats to Outcomes

The most profound threat to Adobe’s digital landlord status is the shift in how software is monetized. For the last decade, the per-seat subscription model was the bedrock of SaaS. However, agentic AI creates a seat-deflation problem. If an AI agent can automate 80% of a creative professional’s tasks, a company may need fewer seats, leading to a massive revenue hit for a vendor that bills per user.

Newer, AI-native companies are adopting usage-based, output-based, or outcome-based pricing models. For example, Intercom charges $0.99 per resolved conversation for its AI agent, rather than a flat monthly fee for access. This aligns the cost directly with the value delivered to the customer.

Adobe’s Defensive AI-Influenced Metric

Adobe has tried to navigate this by introducing Generative Credits, but analysts are skeptical of the AI-influenced ARR metric that management has touted as reaching over one-third of the business. Critics argue that much of this ARR is defensive; it represents existing customers who are paying to retain their seats with added AI features, rather than a massive expansion of new user acquisition.

If AI is merely keeping the seats warm, the high variable cost of LLM inference could actually lead to margin compression rather than expansion. In 2026, 40% of enterprise SaaS contracts are expected to include outcome-based elements, up from 15% just a few years prior. Adobe’s legacy infrastructure, built on desktop-first licenses, makes it difficult to pivot to these outcome models as cleanly as competitors who are born in the cloud-agent era.

The Sora Threat: Disruption of the Professional Video Stack

Nowhere is the AI threat more visible than in the professional video market. Adobe Premiere Pro and After Effects have long been the industry standards for video post-production. However, the emergence of text-to-video models like OpenAI’s Sora, Google Veo, and Luma Dream Machine represents a fundamental shift from editing to generating.

Professional workflows in 2026 are increasingly centered on generative storytelling rather than incremental editing. While Adobe is trying to integrate these models through Adobe GenStudio, it faces a commodity trap.

If a user can generate a photorealistic 1-minute video from a prompt using Sora, the need for a complex, timeline-based editor like Premiere Pro decreases for a significant portion of the marketing and social media content market.

The Productivity Paradox and Market Concentration

While the bull case for Adobe suggests that AI makes designers 10x more productive, the bear case is that 10x productivity leads to a concentration of work into fewer seats. If one designer can now do the work of five, and Adobe still bills per seat, the total addressable market in terms of seats begins to contract.

Furthermore, specialized competitors are picking apart Adobe’s high-margin video features:

Runway Gen-4.5: Offers advanced creative control and cinematic editing that rivals Adobe’s After Effects in speed and quality.

Descript: An AI-first video editor that allows users to edit video by editing the transcript, a workflow that is much more accessible to non-professionals.

Synthesia: Dominates the business and training video segment by allowing users to generate realistic digital avatars from prompts, bypassing the need for filming or traditional editing.

Adobe’s attempt to compete through Firefly Video has been met with mixed reviews. In comparative tests in early 2026, Firefly was noted for its commercial safety but was often seen as lagging in output quality compared to Sora and Google Veo.

Institutional Positioning: The “Smart Money” Exodus

The technical and institutional data on Adobe stock in early 2026 confirms a deep-seated bearishness among professional traders. Short interest in ADBE has reached an eight-year high, and smart money operators have been positioning themselves on the short side through complex options structures.

The stock’s underperformance is stark when compared to the broader market. While the S&P 500 Index rallied 12.2% in the year leading up to February 2026, ADBE shares fell 38.4%. The stock’s Relative Strength Index (RSI) of 29.1 suggests it is oversold, but the persistence of this oversold condition indicates a fundamental regime change in how the stock is being valued.

The Death of the Multiple

Historically, Adobe was valued as a structural winner with a terminal growth rate that justified a high double-digit multiple. Today, that narrative has shifted to one of terminal decay.

Multiple Compression: The TTM P/E ratio of 15.33x is now lower than the average large-cap software peer multiple of 26x.

SaaS Sector Rotation: Institutional investors are slashing software holdings to their most underweight position since 2021, favoring hardware and infrastructure names (like semiconductors and data center REITs) that are seen as the “picks and shovels” of the AI era.

Guidance Skepticism: Management’s target for double-digit ARR growth in FY2026 (10.2%) is being viewed as “optimistic” by many analysts who forecast a trend toward 7-8% revenue growth over the next five years.

Conclusion: The New Paradigm of Agentic Fabric vs. the Legacy Monolith

The synthesis of this research indicates that software is not dead; it is being re-imagined as an autonomous, invisible fabric that enables business outcomes. This shift is highly beneficial for companies that control the integration layer and the data foundation, the agentic middleware that will orchestrate the 21st-century enterprise.

However, for Adobe, the transition is fraught with peril. The company is a monolith in a world of micro-services and vertical agents. Its core advantages—complexity and seat-based licensing—have become its greatest liabilities. The failure to acquire Figma left a multi-billion dollar hole in its UI/UX strategy, while Canva is eroding its base and specialized AI models are disrupting its high-end creative workflows.

Adobe’s current valuation reset to an 11x-15x P/E is not a temporary dislocation but a structural repricing of a company that is no longer a growth leader.

While Adobe remains highly profitable and generates significant free cash flow, its role as the digital landlord of the creative world is ending. The house always wins mathematically in a vacuum, but in an era where the neighborhood is being rebuilt around you, being the landlord of the oldest building on the block is no longer the winning bet.

My bearish outlook on Adobe is a reflection of this reality: the software era is evolving, and Adobe, for the first time in its 40-year history, is on the wrong side of the architectural shift.